Bain survey highlights APAC Private Equity concerns

Findings from Bain & Company’s 2021 annual Asia-Pacific Private Equity Report show the environment remains challenging. Exits were close to a 10-year low and fundraising fell once more.

According to Bain’s survey, conducted with 162 senior market practitioners, the top concerns for General Partners (GPs) surveyed include high valuations, increased competition and the ongoing impact of Covid-19.

Shocked by the fallout from Covid-19, investors initially recoiled but many jumped back into the market, especially in China, India, and Japan. This lifted deal value across APAC to a record high in 2020 of $185 billion – up 19% from 2019.

“It’s been a rollercoaster year for private equity in Asia,” said Kiki Yang, co-head of Bain & Company’s APAC Private Equity practice. “But while dealmaking ended the year on a high, Covid-19 has not gone away, and building portfolio resilience will be a crucial skill for leading investors.”

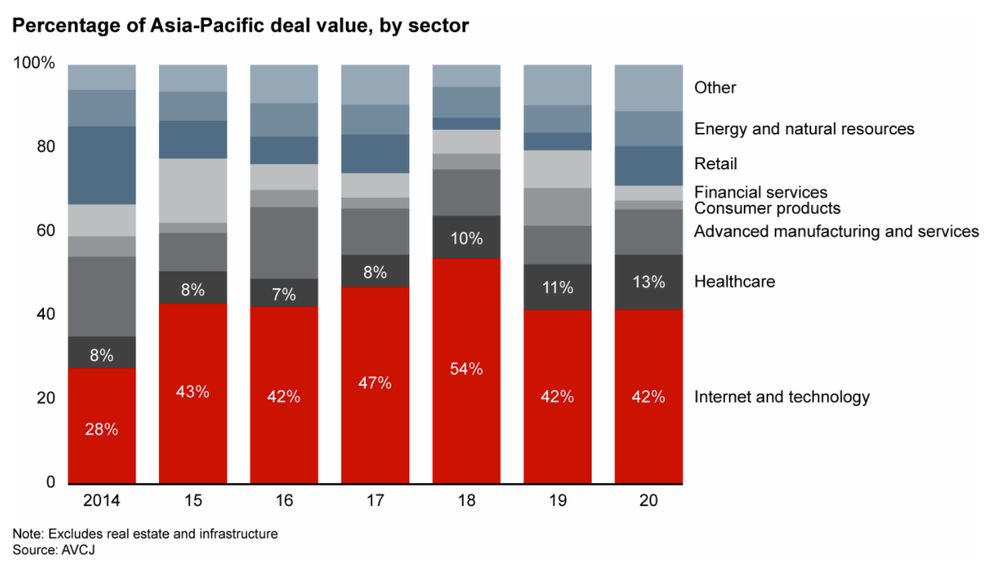

Dealmaking drives PE market

Dealmaking helped the region’s assets under management rise to 28% of the global PE market.

China’s total deal value rose to $97 billion, up 42% from 2019 and 22 per cent higher than the previous five-year average. Meanwhile, India continued to increase its share of deal activity – value rose to $38 billion, up 64 per cent over the prior five-year period.

While deal value also grew in Japan and Australia–New Zealand, South Korea’s deal activity remained flat. Travel restrictions saw deal activity hit hard in Southeast Asia, tumbling by 16% over the previous five-year average.

Investors were quick to seize on those companies who were benefitting from a digital transformation – fast-growing companies with digital business models aligned to the switch to virtual work, education, and retailing.

Following a sharp fall to a 10-year low in 2019, the number of exits was flat in 2020, according to the survey, as PE managers waited for the right time to sell portfolio companies.

Of the GPs surveyed, more than 70% say the exit environment was more challenging than in 2019, with Covid-19 being the obvious main cause.

That said, IPOs dominated the exit market, making up more than 60 per cent by value – which is almost double the previous five-year average. China accounted for 86 per cent of the region’s IPOs, with the majority being healthcare and technology companies.

Fundraising slows in APAC in 2020

Fundraising slowed in 2020, with funds focused on Asia-Pacific raising $90 billion, down 32% year-on-year, and 53% from the prior five-year average. To put that into perspective, global PE fundraising declined only 11%.

According to the survey, 60% of GPs surveyed say top-line growth will be the most important factor contributing to returns in the coming five years, with 56 per cent saying they have a robust value-creation plan in place within the first six months of investment.

What does 2021 hold for APAC private equity?

Nearly 80% of GPs expect the macroeconomic climate to be more favourable this year. Key trends identified include:

- Digital business models will accelerate: In 2020, growth powered ahead in digital businesses. The survey found Asia-Pacific GPs are most interested in investments in digital health, e-commerce, and e-learning.

- Resilience will be a trait of winning investors: Resilience is key to survive and recover from sudden shocks.

“Asia-Pacific has been an exciting and dynamic region for any global private equity fund,” said Andrea Campagnoli, a partner in Bain & Company’s Private Equity practice based in Singapore.

“Improving macroeconomic conditions coupled with many exciting investment opportunities, especially in digitally advanced sectors, will continue to draw strong interest from investors.”

- The importance of shareholder value on Asian societiesLeadership & Strategy

- OAG confirm Kuala Lumpur as #1 connected airport in APACLeadership & Strategy

- Office space demand stronger in APAC than US and EU, reportLeadership & Strategy

- Top 10 airlines in Asia for excellent customer satisfactionLeadership & Strategy